How to break out of a debt spiral

Friends, I want to show you something. See this photo of this adorable 24-year-old idiot drinking cheap sangria at a cafe in the south of Spain?

Well, she might have a smile on her face, but she has a secret.

She's drowning in debt.

Over R200k worth of debt, in fact, which she has no idea how she's ever going to pay off. When she's not taking holidays in Spain, paid for by credit card (which is part of the reason she's in debt, obviously), she's being harassed by debt collectors. She even tried changing her phone number to avoid their calls, but they tracked her down, sneaky debt collectors! Despite the smile in this photo, she's suffering from the kind of depression that makes it hard to get out of bed sometimes. And worse, she is deeply, deeply ashamed. Far too ashamed to ever talk to anyone about what she's going through, or ask for help.

This sweet little 24-year old idiot was me. And going through that dark time is the reason I'm now so passionate about talking to young people about money.

I got into a debt spiral for the most obvious reason: I was living beyond my means. I was terrified of money and felt like I didn't understand it, so I just effectively avoided my debt problem for years and hoped it would go away. Spoiler alert: it didn't! Things only got better when I got honest with myself and decided to face things. I could only do that when I stopped moralising my debt, and seeing it as this terrible crime that I had done that was going to haunt me forever, and took pity on poor silly little past me who didn't know any better.

Debt isn't a moral failing; it's an outcome of our crappy economic system. And you really do have more options than "struggle in silence until things get worse and worse and you can't buy food any more". The fact that you're here, reading this, makes me so proud of you. I don't think you're a fuckup, and I don't think you're doomed to be stuck in debt forever. Far more people are struggling with debt than you realise, they're just not talking about it because they're ashamed, too.

Shame doesn't help anybody. Fuck the shame! Instead, let's make a plan.

What is a debt spiral?

A debt spiral is when your debt repayments get so high that you can't afford your monthly living expenses, so you have to borrow even more money to make it through the month. It's an an ever-worsening spiral of borrowing money to cover your living costs. I'm talking here about high-interest consumer debt, stuff like credit cards, payday loans, personal loans, store cards etc. It often ends up including outstanding bills for stuff like medical expenses, school fees or home loan repayments.

What I'm not talking about here is having a large secured debt in the form of a home loan or business loan, or something like that. Secured debt tends to come at much lower interest rates, and doesn't spiral out of control in the way that lifestyle debt does.

To explain how debt spirals happen, let's turn to our old friends: the snorgles.

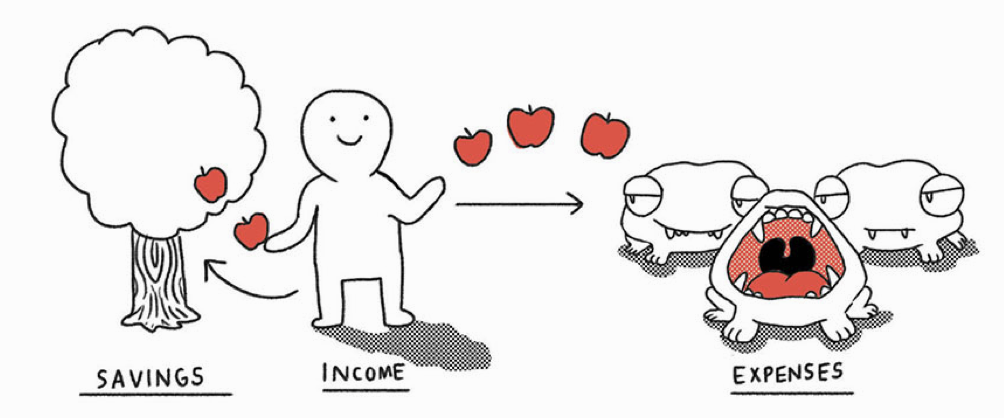

Snorgles are the very adorable little creatures that live in your house and eat up all your money (apples, in this analogy). Each snorgle needs to eat one apple every day, or they'll die. You don't want your snorgles to die! You love those hungry little bastards. So you very diligently go out and pick apples every day to feed them.

If you've got extra apples, you keep them to one side in case you have an apple shortfall sometime in the future.

But here's the problem: most of us never have enough extra apples to save. We can usually only juuuuust get enough apples to feed our snorgles. It might feel like things are going okay! You're making it through the month! Everything's fine!

(Cue ominous background music...)

Inevitably, something goes wrong. You lose your job, and you suddenly have no apples coming in. Or one of your snorgles gets stung by a bee and the vet bills are FRIGHTENING. So you have a shortfall: you need more apples than you have saved. And you can't let your snorgles just die, so you have no choice but to go and borrow apples.

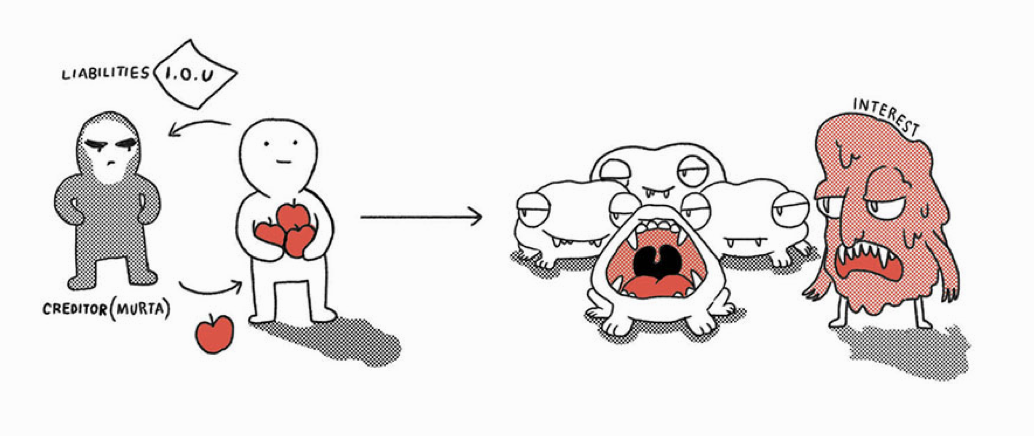

So you go to your creepy neighbour Murta, and ask if you can borrow some of her apples. She loans you some apples, and says you have to pay them back later. That's the simple "I.O.U." part. That's not the problem. The problem is that Murta is not your friend (remember this), so for the privilege of loaning you apples, she says you also have to adopt her gross pet the Interest Monster, and feed it too. For as long as you have the outstanding debt, you have to feed the Interest Monster.

At first, things still seem really good! In fact, having this new line of credit might feel great. It's relieved the stress of having to go and pick all the apples you need every day. Maybe you figure you can even afford to adopt a few extra snorgles. Upgrade one of them to a fancier snorgle breed. And Murta's there the whole time, egging you on, telling you that the debt's totally fine, encouraging you to borrow even more, in fact.

You have to pick some extra apples every day to feed the Interest Monster, sure. But he's not so big, and he doesn't eat so much, so it doesn't feel like an issue.

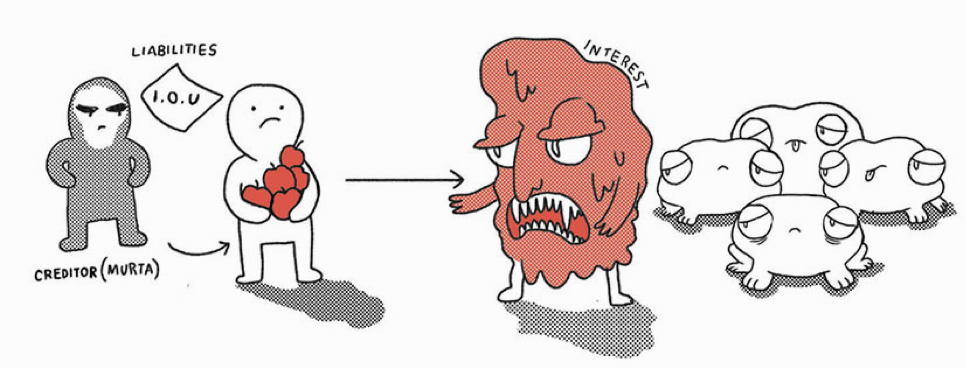

But here's the thing about Interest Monsters: they grow. And the bigger they get, the more apples they need to eat.

And you can still only pick the same amount of apples every day, so now you have a shortage. The Interest Monster is eating so many of the apples that you don't have enough to feed your snorgles.

So now what do you do? You borrow more.

See the problem? In the real world, people usually get into a debt spiral through a series of small decisions, none of which seem so bad in the moment. But there comes a point where on payday, 60-70% of their income goes directly to servicing their debt, leaving them with a paltry 40-30% of their income to live on. And usually, people aren't getting into debt to go on holidays or buy luxury snorgles - they're getting into debt to buy food and pay for basics. In South Africa specifically, people mostly get into debt simply because they can't earn enough money.

And usually, the interest rates on this kind of borrowing is very high, meaning that Interest Monsters grow very quickly.

Once you're in a debt spiral, it is very difficult to get out of it just by Bucking Up and Being Responsible! and any of the other simplistic nonsense that people who have not been in a debt spiral will tell you to do.

Here's what you can do instead:

- Build a DIY debt plan that involves negotiating with your creditors to try to slow down the Interest Monster's growth, and finding extra money to accelerate your debt repayments.

- Enter a formal debt relief process and work with a debt specialist to restructure, pay down or forgive your debts. There are different options in different countries.

Both approaches start with the same first step - getting honest about your debt.

Step 1: Getting Honest

Step one is the least complicated, and the most difficult emotionally: gather up the information about all of your debts, and put them in one place.

For each debt, you need to know:

- Who do I owe this debt to?

- What is the interest rate? To find this out, you might need to call your creditor (the person you owe money to) or check a recent statement.

- How much do you owe?

- What is the minimum monthly payment? If you're not sure, just use the average of whatever you paid over the past 3 months.

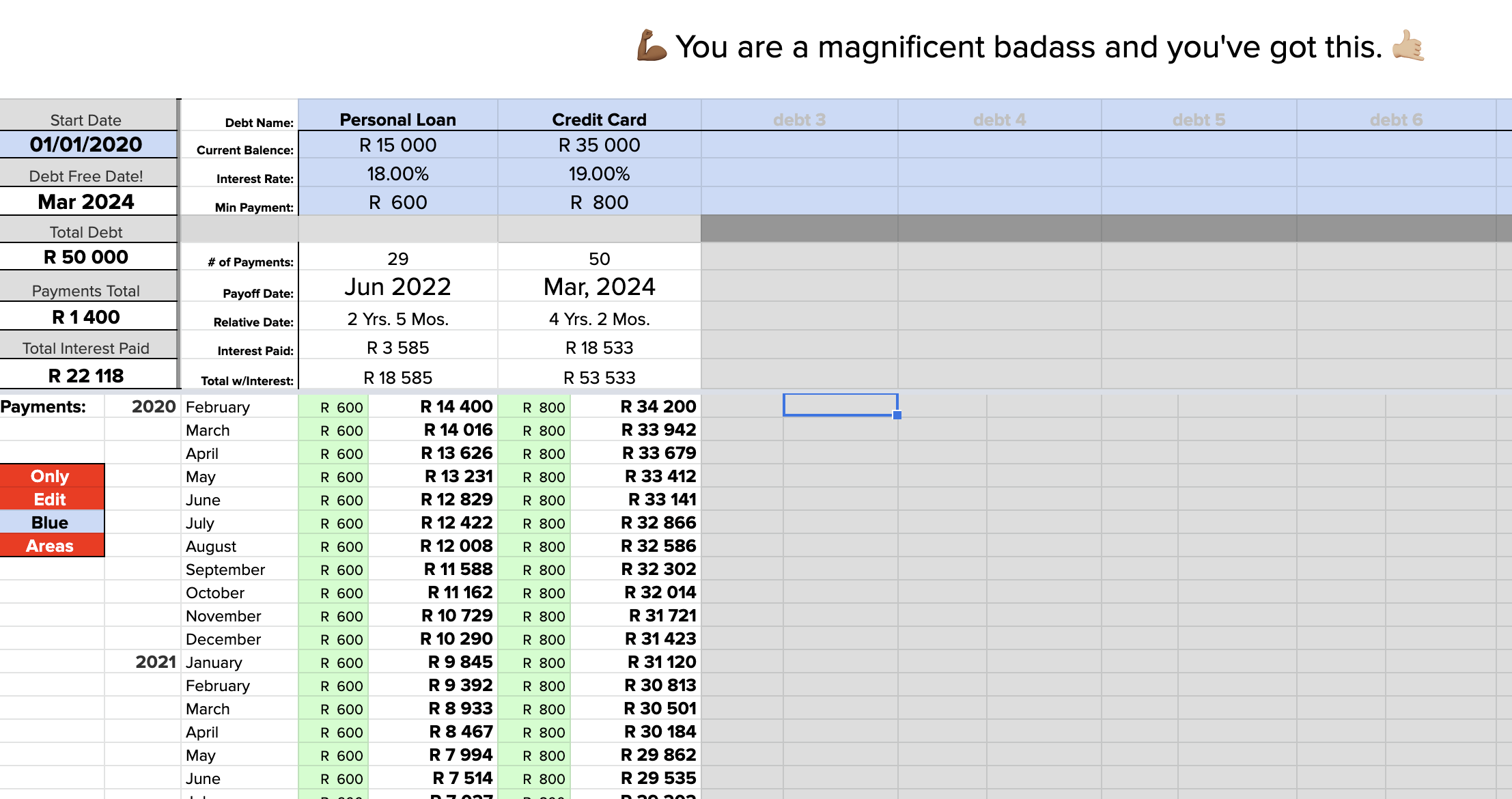

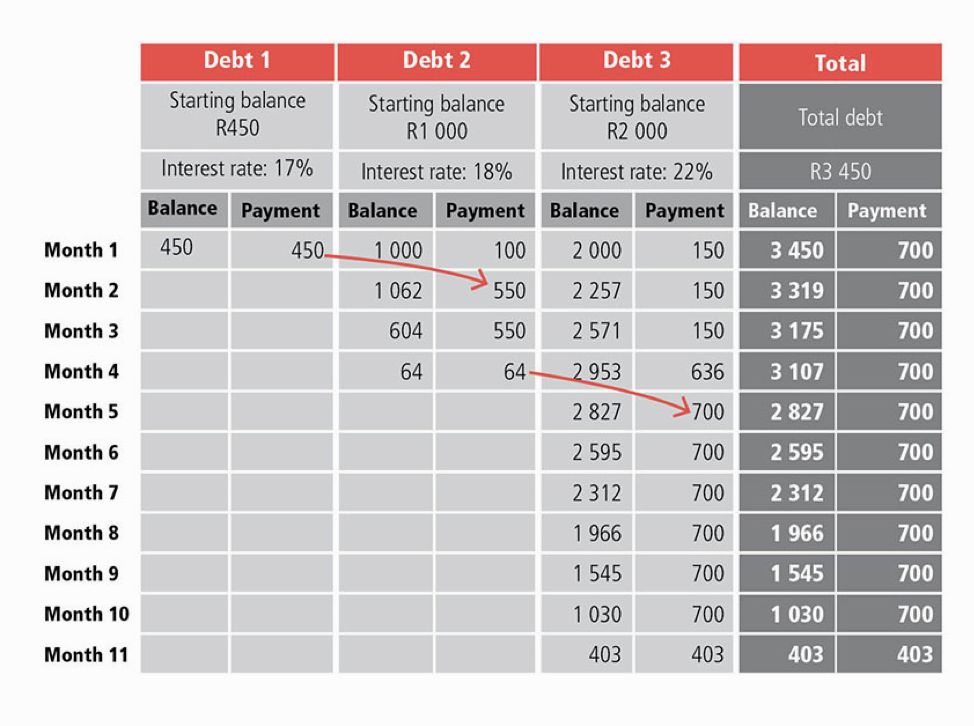

There's a spreadsheet you can use for this. I've created a version in SA Rands, and one in GB Pounds. If you enter in your debts at the top, it will show you when you'll pay down these existing debts at the current rate you're paying them down. Don't be scared when you see this! This is just how things are looking right now, before you start trying to accelerate this.

Just a note: make sure that you are actually responsible for all of these debts. You can't inherit debt from someone, for instance (although you do share your common-law spouse's debts). If you have an old debt that you haven't made payment to for a few years, check whether it has expired (prescribed).

You also need to put together a budget showing where your money is actually going every month. I know, I know, I'm the same person who's always saying budgets don't work. This budget isn't really for you, though. It's a simplified version you're going to send to your creditors or debt counsellor if they ask for it (which they likely will at some point). It's important that this budget is as accurate as you can make it. The best way to get an accurate number is to actually track your spending with an app, or to export your bank statements and go through them in detail.

One more thing you might want to do is get your credit report. You're allowed one free one every year. This might remind you of debts you've forgotten about, and will let you know if you're behind on any payments.

I know these steps suck, buddy. This is a good time to remind yourself that you are not a terrible garbage person, and it's all going to be okay.

Step 2: Put the brakes on

You're stuck in a hole. You need to figure out what to do to get out of the hole. But there's something you have to do first: stop digging.

So, stop taking on more debt. To do that, I'm going to encourage you to do something that seems totally crazy and counter-intuitive: set up an automatic payment that goes into a savings account every month.

I know, mad right?! You're already struggling to make it through the month without turning to debt, and here I am suggesting that you somehow find even MORE money in your budget and put it in a savings account.

But here's why I think you should prioritise saving even when you have high-interest debt: because not having emergency savings is why you took the debt out in the first place.

Emergencies happen. Geysers burst and cars break down. If you don’t have an emergency fund, then the only thing you can do is just go back into debt. And you don't want that. When you stop using debt, it helps if it's a clean break.

So, if you don't have an emergency savings account, go open one. Set up an automatic transfer into it every day on payday. Right now, your goal is 1 month's expenses. In time, you want to build that up, but just aim for a small amount until you've cleared your highest interest debts.

I also want you to fetch all of your credit cards and store cards, take them out of your wallet, and hide them somewhere safe in your house. They're not gone; they're just not easily accessible.

Side-note: you want to close most of your lines of credit once they're paid off, but you should keep your oldest credit card open forever if you can. Having an "old" line of credit will help in the future when you're rebuilding your credit score.

Step 3: Decide what to do

Now that you have the facts in front of you, in black and white, you need to decide whether you're going tackle this yourself, or enter a formal debt relief process. There are pros and cons to each approach.

In South Africa, the most common formal option is debt counselling/debt review.

Pros of debt counselling

- Can help you to protect assets like your house or car.

- Can get mean debt collectors off your back and protect you from legal action by creditors.

- Simplifies your debt repayments: you'll just pay one repayment rather than dozens, and this should be a manageable repayment amount.

- You're not in this alone - you'll get help and advice.

- It's less work than negotiating with your creditors yourself.

- After completing the process, you get a debt clearance certificate which will remove the "debt counselling flag" from your credit history (usually, you can apply for new debt, maybe to apply for a home loan or something, immediately after completing the debt counselling process).

Cons of debt counselling

- It's inflexible - it can be hard to withdraw from the process if your situation changes.

- You won't be able to access new credit during the process (this can be a pro for some people).

- It can cost you more overall (but won't necessarily, and it also could save you money).

- There are a lot of charlatans in this space, so you have to be careful and find someone reputable.

- Not everybody qualifies (for instance, you have to have a stable income).

- It won't protect you if there's already legal action against you.

As a general rule of thumb, if you've already trimmed your spending to the bone and you're still not coping because of your debts (as in, you can't make it to the end of the month without borrowing), then go for debt counselling. If you feel like there's probably still room for you to earn more, or just be a bit more disciplined with your spending, you might want to try handling it on your own first. But you should do your own research and go with your own gut on this.

If you decide to go the formal route, contact a reputable debt company and start the process. You'll have all the information you'll need in the spreadsheet you put together: good on you! PLEASE be careful and use a reputable business, because you do hear horror stories. In South Africa, the only company I've personally heard recommendations of is Debt Busters. You can also look at the Debt Review Awards winners.

In the UK, there are a few different options ranging from getting a debt management plan to a debt relief order. Your best bet is to contact a debt charity like the National Debtline or Stepchange.

Here's a debt story from one of our readers, who very kindly agreed to share their debt review story with all of you (thank you, lovely reader)!

I became over indebted for a few reasons – I had an unstable income, about half of it came from commission which fluctuated from month to month, and I was definitely living beyond my means (however, in retrospect I don’t think it would have been possible to live fully within my means on that one income) and it felt like the bank I was with, FNB, was always trying to give me credit. I remember those few years as being very chaotic and stressful, with credit cards, personal loans and payday loans (from FNB, Wonga, Boodle). I was also travelling internationally a lot for work, and while the main costs were paid for, there were a lot of costs I had no business paying too. Also not sure how I used to find the money to go out to bars a few times a week as well?

I can’t remember exactly why I decided to go with debt review, but I think the final catalyst was that I was probably broke, and had applied for a Wonga or a Boodle and been declined. I think up until then, I was just playing catch up, and it had all caught up with me. I probably just Googled and Debt Busters was the one that came up. The process was super easy: I sent an online enquiry and they called me back. They did it all over the phone, and were able to see most of my debts on their system, which was great, because I was in extreme denial about what I owed. It was probably only about R90k but I was drowning in the different payments. They calculated what I could afford to pay each month, and then worked out a 5 year repayment plan. I think they got most of my interest down to zero, and one loan was at 0.9%. It halved my monthly payment, and more important, it meant that I could not access any new credit.

About a year later I got a new, higher paying job and a while later I increased my payment and I finished the process after four years.

It was a sacrifice for sure. There were many occasions over the 4 years when I could have used access to credit, like when a previous employer just randomly withheld my last month’s salary or when I moved to another city on a whim. But, I survived. I don’t have wealthy parents to bail me out, but I am lucky that I could rely on them in an emergency as well as some very supportive friends. At the end of the day though, I’m still here and it wasn’t THAT bad.

The best part is the feeling of being in control of my finances. It was just always so chaotic before and extremely stressful. A lot of my money anxiety and fear is gone. I would swipe away those bank SMSes and almost never open my banking app. I also changed banks to Capitec at the time (recommended by Debt Busters, as creditors will still try to pull your old debit orders even if you are under debt review) and I am SUPER happy with them. They never try to get me to take out a credit card!

I found Debt Busters to be empathetic, super helpful and reachable throughout the process.

I got my clearance certificate in October last year, and I was on holiday in Japan at the time the email came through, which I was able to pay for without any credit so it was a really great feeling.

I have accessed some credit since then without any problem – I know people often have trouble with this after being on debt review. And it really does depend on who does it for you. I have heard nightmare stories of terrible debt counsellors, but I was one of the lucky ones I guess.

All in all it was such a positive process, and it feels so good to get my salary and have it all be mine.

The DIY route

Step 3a - negotiate with your creditors

The first thing you want to do is to try to negotiate with your creditors. I know, when you're overwhelmed with debt, your creditors are the LAST people you want to talk to. But honestly, your best chance is to approach them politely and proactively as soon as you have a problem, before you start missing payments, ideally.

Explain your situation, and ask how they can help you. It's in their own best interests to get some money from you rather than no money, so they are incentivised to help you! Here is a rough script you can use when calling your creditors to ask for help. Potential solutions you can discuss with them:

- Would you be willing to reduce the interest rates on my loans?

- Would you be willing to give me an interest-free payment holiday until my temporary situation changes?

- Would you be willing to write off a portion of the debt in exchange for a partial payment?

It's helpful, when assessing your options, to remember the general rule about Interest Monsters: the longer it takes you to pay back a debt, the more interest you pay overall. Your creditors might offer to restructure your debts by letting you pay a lower monthly payment and extending your debt over a longer period. Avoid doing this if you possibly can.

Here's an example. Imagine you have a R10,000 loan at 20% interest.

- Pay off R500 a month for 23 months = you pay R12,018 in total.

- Pay off R800 a month for 12 months = you pay R11,099 in total.

- Pull money out of your home loan (10% interest) to pay it off over 10 years = you pay R13,442 in total.

Another option you can consider is applying for a consolidation loan, where you bundle all your debts into one debt that hopefully has a lower interest rate. It's worth getting a couple of quotes for this. Plug in the details of your consolidation loan offer into the spreadsheet and check whether you'll end up paying more overall than sticking to your current loans.

Do not cash out your retirement savings to pay down consumer debt. But if you have extra savings (beyond your emergency fund) you should consider putting it towards your debts.

Step 3b - free up extra cash

If you're drowning in debt and you're serious about getting out of it, it's time to sit with your budget and ruthlessly cut back anything you can live without (i.e. cull some snorgles). This is all the boring, tedious work of getting competitive insurance quotes, downgrading your car and other such glamorous steps, but every cent matters. There are a bunch of money-saving ideas in the book. My advice is to start with the big 3: where you live, how you get around, and the food you eat.

You also need to give some thought to your income. Can you ask for a raise? Can you start a new side hustle?

Here's another wonderful reader who agreed to share their story. They went the DIY route.

So I have managed to (almost) pull myself out of some fairly large debt (although it's apparently small compared to other stories I hear), and I've done this during the lockdown in which I got a 50% pay cut! Here's how I'm doing it.

Before Covid (BC) I was just scraping through on my salary, and my credit card was maxed out, so every month I'd make the minimum payment into the card, and then spend it in the course of that month... well, what was left after the hefty interest charge came off!

Then in May we were given the bad news that we were getting 50% salary cuts. I went into full emergency mode and organised payment holidays on my car and bond - 2 of my 3 biggest expenses every month, the other one was medical aid who weren't offering payment holidays the bastards!

I then luckily managed to get some freelance work on Saturdays which paid enough to cover the salary shortfall. But with the payment holidays in place I was actually coming out with more money each month than in my normal BC life. And I put every extra Rand into the credit card every month... and in 5 months I've paid off half of my R40k credit card debt, while actually living decently and eating sushi as often as I want. Have to reward my 6-day work week somehow right?

So ja, for me there was no easy way out - had to give up half my weekend, but I have to say it's been worth it.

Step 3c - stick to it

Something really magical happens when you start paying down debt. Once you've paid off your first debt, the repayments you were making on that debt are suddenly freed up, so you can put them towards the next debt, and pay them off faster than you thought (that's what the spreadsheet will show you). Your debt repayments become like a snowball picking up more and more momentum, until they are UNSTOPPABLE.

If you're drowning in debt, try to pay down the smallest debts first (the "snowball method") - this will give you an early psychological win. There's something SO DAMN SATISFYING about clearing a debt, closing that account, cutting up that damn card, and being a little more free than you were yesterday.

(Sidenote: you usually have to actively CLOSE an account once you've paid it off, by calling them - they don't close most paid off debts automatically. Sidenote on the sidenote: remember not to close your oldest credit card account because it helps your credit history.)

Good luck out there 💪🏾

Phew, what a post!

There is a wonderful side-effect of having been in a debt spiral, and have broken yourself out of it: you've learned how to live without a chunk of your income every month. I think reformed debt-spirallers sometimes end up being better savers in the end, and more likely to ultimately work towards financial freedom.

I am so proud of you for making it here, and I wish you all the damn luck in the world.

CONQUER!

Your questions about debt review

Update 15 April 2021: after publishing this piece, I received a couple more questions about debt review. I reached out to Benay Sager, the head of DebtBusters, for his expert responses.

If one applies for debt review does it not affect your chances of getting a new job of ones prospective employer does a credit check?

The short answer is, it should not affect one’s ability to get a job. The long answer is, it is a matter of decision or consideration for the prospective employer.

If a consumer is under debt review, there will be an indicator on the credit bureau stating that. As a result, a credit check would indicate the consumer is under debt review.

In the past eight years that I have been involved with DebtBusters, we helped thousands of consumers. I can recall only two or three instances where consumers were told by prospective employers that “due to the nature of the work they were being interviewed for, they would not hire someone who is under debt review” – the few instances were in the financial services industry for jobs that required the individual to handle money or deal with financial matters. An employer is of course free to make such a choice (based on the nature of the work), however the consumer cannot be automatically denied employment just because they are under debt review.

In my view, consumers who choose debt review should – if anything - be rewarded: one would argue that a consumer who has voluntarily recognized and taken steps to improve their financial situation should be applauded instead of being prejudiced against.

If under review and I get a lump sum of cash am I allowed to pay it off quicker without the “interest”?

Definitely. This happens quite regularly, and consumers are encouraged to contribute more if they can. A great debt counsellor should negotiate interest rates down for the consumer in any case, so any extra contribution will help repay the outstanding capital amount.

Can one rent a new flat or will the agent also do a credit check and not approve?

The answer to this question is similar to the employment one. For a consumer who is under debt review, a credit check would return the result that a consumer is under debt review. If the agent and/or owner decide to not rent the property to the consumer as a result of the credit check, that is purely their decision. With that said, the consumer who is up to date with their payments can ask for a reference letter from the debt counsellor indicating they are under debt review and are making debt repayments regularly. We have issued such letters in the past and find them to be very helpful.

Member discussion